July 31, 2014

Earnest Money Deposit as Liquidated Damages

Your typical disputes over an earnest money deposit as liquidated damages in residential real estate sales go something like this: Home buyers decide to submit a contract and an earnest money deposit as an offer to purchase the property. Before closing, the buyer cannot find financing or discovers a defect with the home. If the buyer still has a contingency she can exercise to get out of the contract, then usually there is not a problem with return of the deposit. Where the seller is worried about finding another buyer and there is no applicable contingency, there might be a dispute over who is entitled to the escrowed funds. In scenarios falling within this classic dilemma, the common fact is that the realtor, seller or some other escrow agent holds the buyer’s funds until they are dispersed pursuant to the sales contract.

Your typical disputes over an earnest money deposit as liquidated damages in residential real estate sales go something like this: Home buyers decide to submit a contract and an earnest money deposit as an offer to purchase the property. Before closing, the buyer cannot find financing or discovers a defect with the home. If the buyer still has a contingency she can exercise to get out of the contract, then usually there is not a problem with return of the deposit. Where the seller is worried about finding another buyer and there is no applicable contingency, there might be a dispute over who is entitled to the escrowed funds. In scenarios falling within this classic dilemma, the common fact is that the realtor, seller or some other escrow agent holds the buyer’s funds until they are dispersed pursuant to the sales contract.

What if the buyer signs the contract but never submits the deposit and does not go to closing? Can the buyer still be liable to the seller in the deposit amount? The Circuit Court of Fairfax County, Virginia, recently held that contract default language in a National Association of Realtors form was unenforceable as written under this scenario.

In April 2012, Sagatov Builders, LLC entered into a contract to sell Christian Hunt a residential property in Willow Creek Estates in Oakton, Virginia. The contract required Mr. Hunt to submit a $50,000 deposit within 5 days of the issuance of the building permit. The seller submitted the approved building permit to Mr. Hunt in September 2012. According to the Complaint, Mr. Hunt failed to make the deposit or to go to closing. According to Redfin.com, the property was sold on Dec. 13, 2013 for $2,775,000. Perhaps Sagatov suffered some expenses and inconveniences associated with having the property tied up with Mr. Hunt during peak home selling months. Sagatov’s website has an advertisement for the completed property, including pictures and a description. In April 2014, Sagatov Builders filed a lawsuit against Mr. Hunt for the unpaid $50,000.00 deposit as liquidated damages for his breach of the contract.

Why is Sagatov seeking the deposit amount as liquidated damages instead of a calculation of actual damages suffered? The parties used a National Association of Realtors Sales Contract for Land form No. W-48C (VA) dated 6/95. Section 21, entitled, “Default,” provides that:

If the Purchaser is in default, the Seller shall have all legal and equitable remedies, retaining the Deposit until such time as those damages are ascertained, or the Seller may elect to terminate the contract and declare the Deposit forfeited as liquidated damages and not as a penalty …. If the Seller does not elect to accept the Deposit as liquidated damages, the Deposit may not be the limit of the Purchaser’s liability in the event of a default.

On its face, this provision would seem to give the seller the option of retaining the deposit as liquidated damages and/or going after the buyer for additional damages. What are “Liquidated Damages” in Virginia? Attorney Lee Berlik defines them in his blog post as:

[T]he amount of which has been agreed upon in advance by the contracting parties. When a contract contains a liquidated-damages provision, the amount of damages in the event of a breach is either specified, or a precise method for determining the sum of damages is laid out. This is often done in situations where the parties agree that the harm likely to be caused by a breach would be difficult or impossible to measure with any precision, so they agree on a figure in advance and dispense with the time and effort that would otherwise be involved in proving compensatory damages at trial.

Rather than litigating a hot mess of damages issues, parties can stipulate to liquidated damages in their contracts. So long as the liquidated amounts are not deemed a “penalty” by the Court, these provisions are enforceable. A few months ago I posted an article to this blog about how Courts seek to avoid imposing similar penalties in construing commercial lease acceleration of rents provisions.

The liquidated damages provisions in the real estate form that came before Fairfax Circuit Court Judge Charles Maxfield presented a new twist on the liquidated damages vs. improper penalty debate. Upon the buyer’s default, these provisions gave the Seller the option of electing the liquidated damages or seeking some other amount of damages.

Judge Maxfield declared the liquidated damages option in the contract to be unenforceable because:

- It isn’t a true stipulation to liquidated damages because of its elective characteristics; and

- Even if it was, it is a “penalty” because it would only be exercised if actual damages were less than the deposit amount.

I think that the drafters of the form (leaving aside for a moment the changes made by Sagatov and Hunt) contemplated that an escrowed deposit would become a potential source for payment of damages in the event of default. These default terms seem focused on avoiding a scenario where the escrow agent would have to release the deposit, only to watch an aggrieved party chase after those released funds in court. They seem to have tried to create a right to draw on an escrow in the event of a breach.

Virginia Lawyers Weekly reports that Sagatov will have an opportunity to re-draft its pleadings based on the Court’s ruling. It will be interesting if this case ultimately goes up on appeal to the Supreme Court of Virginia.

If the $50,000 deposit had been actually escrowed, would the Court’s interpretation and application of these Default terms be any different? If actual damages were less than $50,000, would drawing the whole amount constitute a “penalty?” What if expenses dealing with the dispute, such as attorney’s fees, were incurred by the seller?

{kind=link}

July 24, 2014

Tenancy by the Entirety and Creditor Recourse to Marital Real Estate

Last week I focused on first-time home buyers and new opportunities for state tax-exempt estate planning. This week’s post continues on the theme of family. Spouses who own Virginia property together may enjoy special protections against the claims of their individual creditors. This special form of ownership is called “Tenancy by the Entirety.” For this to arise, the husband and wife must own in unity of (a) time, (b) title, (c) interest and (d) possession. These requirements may be inferred if the deed specifically conveys to the husband and wife by tenancy by the entirety or with an intent to create a right of survivorship.

As far as creditors are concerned, the couple jointly owns an undivided 100% interest. This ancient doctrine continues to be applied by Virginia courts in contemporary real estate controversies. This post focuses on ways creditors may succeed in spite of this manner of holding title:

- Joint Consent. Neither spouse may sever the tenancy by his sole act. Likewise, one spouse cannot convey the property unilaterally. This becomes significant if one spouse attempts to mortgage the property without the consent of the other. However, the spouses may cause the termination of the tenancy by the entirety ownership or jointly liability for a lien or judgment. For example, when the owners take out a mortgage, if properly perfected, that lien will persevere against acts of divorce and/or bankruptcy unless exceptions apply. Also, if only one spouse files for bankruptcy, the tenancy by the entirety property remains outside of the Bankruptcy Estate.

- Divorce. Completion of a divorce transforms a tenancy by the entirety into a tenancy in common, the ordinary form of co-ownership. In equitable distribution, a Judge has considerable latitude in dividing up marital property.

- Death. Because of the right of survivorship, no transfer of title occurs to the survivor upon the death of a spouse. Upon death, the interest of the surviving spouse converts from a tenancy by the entirety to a sole ownership interest. At that time, the property then becomes subject to creditor claims.

- Fraud. If the husband and wife attempt to work a fraud on a creditor by improper use of a tenancy by the entirety conveyance, it is unlikely that the court would permit the fraud. However, if the couple sells real estate held in a tenancy by the entirety, the proceeds of that sale automatically also enjoy the same status as the real estate, unless there is an agreement to the contrary. A transfer from the husband and wife holding in tenancy by the entirety to the sole name of one of the spouses does not subject those funds to the claims of the other spouse’s creditors.

The gist of tenancy by the entirety flows intuitively from the legal understanding of marriage. It possesses a seemingly “magical” quality when it comes to protecting against many individual creditor claims. However, it can be difficult applying the doctrine to a family’s individual circumstances. If you have questions about Tenancy by the Entirety, whether as a spouse or a creditor, contact a qualified attorney.

Court Opinions:

In Re Eidson, 481 B.R. 380 (Bankr. E.D. Va. 2012) (interpreting Va. law).

Alvarez v. HSBC Bank USA, 733 F.3d 136 (4th Cir. 2013) (interpreting Md. law).

U.S. v. Parr, File No. 3:10-cv-061 (W.D. Va. Oct. 6, 2011) (Moon, J.) (interpreting Va. law).

In Re Bradby, 455 B.R. 476 (Bankr. E.D. Va. 2011) (interpreting Va. law).

In Re Nagel, 298 B.R. 582 (Bankr. E.D. Va. 2003).

{kind=link}

July 11, 2014

The California Nanny and Mediating Legal Disputes Through the Media

Marcella and Ralph Bracamonte brought Diane Stretton into their Upland, California home to provide childcare services in exchange for room and board. Ms. Stretton and the Bracamontes got into a dispute over their arrangement. Ms. Stretton stopped working and refuses to move out. Why is this story national news? The answer illustrates some pitfalls of mediating legal disputes through the media. Parties are better off resolving seemingly intractable disputes through judges, qualified mediators and experienced attorneys.

Every day, disputes arise over the treatment, performance and compensation of employees. Most states have employment commissions to alleviate stress on the court system. Disputes over how soon a landlord is entitled to have a non-paying tenant depart are also commonplace. Many courts even have special hearing days for evictions. Diane Stretton has been dubbed the “Nanny from Hell,” “Nightmare Nanny” or “Won’t Go Nanny.” Why has her story captured our attention?

In March 2014, the Bracamontes family hired Ms. Stretton off CraigsList to be a live-in nanny for their three children. Over the next three months, the relationship deteriorated. According to the Bracamontes, Stretton stopped working and continued to occupy the premises after they fired her on June 6th. See Jul. 8, 2014, J. Hayward, “Nanny from Hell and the Squatter Ethos.”

Ms. Stretton maintains that as the weeks progressed, Marcella Bracamonte demanded additional tasks of her far beyond their original arrangement. When someone isn’t getting paid their wages and doesn’t like the work, usually they simply quit and go home. For Stretton, the workplace was home. Ms. Stretton stayed despite the couple’s demands. On June 25th, they served her with legal notice in the living room of the residence.

No Self-Help Eviction. In California, like Virginia, once someone makes a property their residence and declines to leave voluntarily, the owner cannot evict them without going to court. Each state has a different housing code. Some are more friendly to landlords, others favor tenants. The common principle is that in the event of a dispute, the resident cannot be booted out without legal action. All of us sleep better at night knowing that we have a right to due process before a mortgage lender or landlord attempts to remove us from our home.

Boundaries are Good. Both the Bracamontes and Stretton voluntarily entered into this living & working arrangement as strangers without establishing significant boundaries. The Bracamontes not only consented to have Stretton care for their children, they also agreed to allow her to live with the family. On the level of human intimacy, this high on the trust scale.

Stretton is also vulnerable. She isn’t being paid a salary and relied on her “host” family for food, water, shelter, etc., in exchange for her labors. Tom Scocca of Gawker sees an element of exploitation on the part of the Bracamontes, characterizing them as seeking a live-in nanny while ignoring California’s wage & hour laws. After the situation deteriorated, they went to the media, complaining that their unpaid servant will neither work nor leave. Jul. 3, 2014, T. Scocca, “The ‘Nanny from Hell’ is an American Hero.”

A written lease agreement sets out the remedies available to the parties in the event of a default of specific obligations such as paying rent. However, the document performs another role. Even if the parties had entered into a thorough legal contract, Stretton still would be entitled to have her case heard by a judge, a process that could take several weeks or months, depending on the jurisdiction. Experienced landlords and employers know that a written agreement does not guarantee that the tenant or employee will perform according to that document. A written lease agreement is a legal instrument, but it is also an opportunity to define boundaries of human relationships at the time they form. For the Bracamontes and Stretton, those dynamics stretch both professional and personal boundaries. If the lease and employment agreement negotiation process had been conducted properly, this whole situation may have been avoided in the first place.

Counterproductive Media Attention. According to a July 9, 2014 People.com article, Stretton’s belongings still remain at the Bracamonte’s house. Although she is no longer sleeping there, she has declined to move out until conditions are met. She is unhappy that the news media is camped out around the Bracamonte house. To move she would have to run gauntlet of cameras and microphones in the hot sun. Some reports indicate that she suffers from health complications. As I mentioned earlier, eviction and employment termination disputes are common. News outlets don’t normally monitor them. Did the family or the nanny instigate the media attention to their case? The Bracamontes are no longer making appearances with CBS2 because the family now has an Exclusivity Agreement with another media network. Jul. 9, 2014, CBS2, “Controversial Nanny Tells Her Version of Events.” In the other ring of the circus, Stretton provided a “mountain of paperwork” to People magazine supporting her position. If the Bracamontes had simply gone to court like other landlords reaching an impasse, perhaps Stretton would have left of her own accord by now. Perhaps they fear a counterclaim. The parties decisions to interact with each other through the media has escalated the conflict in a mutually detrimental way. The media presence must have an effect beyond deterring the nanny’s move. I imagine news trucks interfere with day-to-day family life.

I hope for the sake of those three kids, Ms. Stretton gets a reasonable opportunity to remove her belongings from her room. Once the TV trucks leave, the adults can resolve their monetary claims. Bracamonte v. Stretton illustrates the risks of presenting a legal dispute to the news or social media rather than in court or at the settlement table.

photo credit: fredcamino via photopin cc

{kind=link}

July 2, 2014

Attorneys Fees for Rescission of Contracts Obtained by Fraud

In lawsuits over real estate, attorney’s fees awards are a frequent topic of conversation. In Virginia, unless there is a statute or contract to the contrary, a court may not award attorney’s fees to the prevailing party. This general rule provides an incentive to the public to make reasonable efforts to conduct their own affairs to avoid unnecessary legal disputes. An exception to the general rule provides a judge with the discretion to award attorney’s fees in favor of a victim of fraud who prevails in court. Effective July 1, 2014, a new act of the General Assembly allows courts greater discretion to award attorneys fees for rescission of contracts obtained by fraud and undue influence. The text reads as follows:

This new statute narrowly applies to fraud in the inducement and undue influence claims requesting as a remedy rescission of a written instrument. I expect this new attorney’s fees statute to become a powerful tool in litigation over many real estate matters.

- Obtaining Approval of Written Instruments by Misconduct. This new statute does not focus on the manner or sufficiency of how obligations under a contract or deed are performed. Instead, it concerns remedies where one party obtains the other’s consent on a written instrument by material, knowing misrepresentations made to induce the party to sign (fraud) or abusive behavior serving to overpower the will of a mentally impaired person (undue influence). Fraud and undue influence are usually hard to prove. There are strong presumptions that individuals are (a) in possession of their faculties, (b) are reasonably circumspect about the deals and transfers they make and (c) read documents before signing them. This new statute does not allow for fees absent clear & convincing proof of the underlying wrong. Tough row to hoe.

- Undoing Deals Predicated on Fraud or Undue Influence: This new statute doesn’t help plaintiffs who only want damages or some other relief. The lawsuit must be to rescind the deed or contract that was procured by the fraud or undue influence. Rescission is a traditional remedy for fraud and undue influence, and it seeks to “undo the deal” and put the parties back in the positions they were in prior to the consummation of the transaction. This statute should give defendants added incentive to settle disputes by rescission where a fraud in the inducement or undue influence case is likely to prevail.

- Reasonableness of the Attorney’s Fees Award: When these circumstances are met, the Court has discretion to award reasonable attorney’s fees. Note that the statute does not require that fees be awarded in every rescission case. Under these provisions, on appeal the judge’s attorney’s fees award or lack thereof will be reviewed according to the Virginia legal standard for reasonableness of attorney’s fees.

Prior to enactment of Va Code Sect. 8.01-221.2, defrauded parties had to meet a heightened standard in order to get attorney’s fees. In 1999, the Supreme Court of Virginia held in the Bershader case that even if there is no statute or contract provision, a judge may award attorney’s fees to the victim of fraud. However, in Bershader the Court found that the defendants engaged in “callous, deliberate, deceitful acts . . . described as a pattern of misconduct. . .” The Court also found that the award was justified because otherwise the victims’ victory would have been “hollow” because of the great expense of taking the case through trial. The circumstances cited by the Court in justifying the attorney’s fees award in Bershader show that the remedy was closer to a form of litigation sanction than a mere award of fees. Bershader addressed an extraordinary set of circumstances. Trial courts have been reluctant to award attorney’s fees under Berschader because it did not define a clear standard.

The new statutory enactment removes the added burden to the plaintiff of showing extraordinary contentiousness and callousness or other circumstances appropriate on a litigation sanctions motion. It is hard enough to prove fraud or undue influence by clear and convincing evidence, and then show reasonableness of attorney’s fees. Why should the plaintiff be forced to prove callousness and a threat of a “hollow victory” if fraud has already been proven and the court is bound by a reasonableness standard in awarding fees? The old rule placed a standard for awarding attorney’s fees in fraud cases to a heightened standard comparable to the one available for imposition of litigation sanctions. Va. Code 8.01-221.2 permits attorney’s fees in a rescission case without transforming every dispute in which deception is alleged into a sanctions case.

case citation: Prospect Development Co. v. Bershader, 258 Va. 75, 515 S.E.2d 291 (1999).

photo credit: taberandrew via photopin cc (photo is a city block in Richmond, Virginia and does not illustrate any of the facts or circumstances described in this blog post)

{kind=link}

June 18, 2014

Contesting Foreclosure In Bankruptcy Court

Can a homeowner block a foreclosure by filing for bankruptcy protection immediately after the bank-appointed trustee auctions the property? On June 2, 2014, a bankruptcy court judge ruled that Rachel Ulrey’s Roanoke property was not excluded from the bankruptcy estate because the foreclosure trustee completed the memorandum of sale prior to the court filing. The court opinion is of interest to homeowners facing foreclosure, mortgage investor or buyers at foreclosure sales. The case illustrates what can happen when a borrower is contesting foreclosure in bankruptcy court.

Rachel Sue Ulrey lives in Roanoke, Virginia. She fell behind on her payments to Suntrust Mortgage. Suntrust instituted foreclosure. Timothy Spaulding, the foreclosure trustee, conducted the sale on the steps of Roanoke Circuit Courthouse at 9:45 A.M on April 18, 2013. Suntrust submitted the only bid of $98,275.52. To memorialize the sale to Suntrust, Spaulding inscribed the details on the bidding instructions form.

About 45 minutes later, Ms. Ulrey filed for protection from creditors pursuant to Chapter 13 of the Bankruptcy Code. Unlike a Chapter 7 where the debtor’s estate is liquidated and the unsatisfied debts are discharged, in Chapter 13 the debtor has the opportunity to present a plan to reorganize and pay off existing debts according to a plan approved by the bankruptcy judge. This presents an opportunity to keep significant assets such as cars and homes.

Ulrey put Suntrust on notice of the bankruptcy case and presented a plan which the Court confirmed by an order entered July 12, 2013. Ulrey wanted to work out her arrearage with Suntrust and keep her home. Ulrey even made electronic mortgage payments in May – July 2013 to Suntrust. The bank returned these payments into Ulrey’s checking account.

Suntrust and Ulrey litigated in Bankruptcy Court over the validity of the foreclosure sale and whether the homeowner could make keeping the home part of her Chapter 13 Plan. The Court decided that because Suntrust never contested Ulrey’s bankruptcy plan, the bank is bound by that order. However, there is a catch – Ulrey must make sufficient payment to the bank to bring her plan current within 30 days. Otherwise, the Bank can proceed against the Ulrey house. Ulrey is both protected and bound by her reorganization plan. How can the Court find the foreclosure sale to be valid and then go on to enforce the bankruptcy plan treating the property as part of Ulrey’s estate? Doesn’t it have to validate one and void the other? The answer provides an expansive vision of bankruptcy jurisdiction:

Formality Requirement for a Written Memorandum of Foreclosure Sale: The Memorandum of Sale in foreclosure is comparable to a Regional Sales Contract in an ordinary deal. They both give the buyer a contractual right to later exchange the purchase price for a title deed. However, most Memoranda of Sale do not contain detailed contractual provisions. The one in Ulrey was a one page form containing the basic identifying facts of the sale and the bank’s bidding instructions. Ulrey challenged the validity of this document on the grounds that it did not contain enough terms. The sufficiency of the memorandum is legally significant. Contracts for sale of real property generally must be in writing to be enforceable. The Court suggests that Spaulding actually included more information in the Memorandum than was necessary to make it enforceable. The terms of the Memorandum of Sale are the business of the trustee and the buyer in foreclosure because they set a framework for going to closing. Whether the memorandum contains particular warranties or descriptions is not the prior owner’s issue.

Legal Rights of Homeowner Post-Foreclosure: If the foreclosure sale produced an enforceable contract between the trustee and the buyer, how does Ulrey have standing to put the property into her Chapter 13 Plan? The Court observed that post-foreclosure there were litigatible issues over the validity of the sale and Ulrey’s continued occupation of the premises. Without filing for bankruptcy, Ulrey could have tried to sue Suntrust challenging the foreclosure or opposing the eviction proceeding. These “residual” legal rights brought the dispute over the property into the jurisdiction of the bankruptcy court. The Court does not discuss whether Ulrey could have properly set forth a nonfrivolous claim contesting the foreclosure proceeding. It is one thing to have a lawsuit that could be filed and it is another to have one that could go to trial and possibly win. The Court implies that Suntrust waived that issue.

Power of Bankruptcy Court Orders Confirming Chapter 13 Plans: Although the memorandum of sale was valid, Ulrey succeeded in putting the ball back in Suntrust’s side of the court by filing a bankruptcy plan that included keeping the home. Ulrey got another opportunity to keep the home, because Suntrust failed to object to the bankruptcy plan. Ulrey succeeded not because she discovered a legal trick to successfully block a foreclosure. Rather, she got another bite at the apple because Suntrust failed to pay attention to her bankruptcy case. Ulrey’s case stands as a warning to mortgage investors to not ignore the owner’s post-sale bankruptcy filing, even when the foreclosure is conducted properly.

Hopefully for Ulrey she can come current on her bankruptcy plan and continue to make her mortgage payments. However, the Court states that Ulrey suffered a job loss and drained her bank accounts to pay living expenses. Her case illustrates the fleeting nature of successful foreclosure contests.

If Ulrey doesn’t come current, does Suntrust proceed with eviction or does the bank have to conduct a foreclosure sale again beforehand? Since the Court found the sale to be valid, perhaps re-auctioning the property would be unnecessary.

Case Citation: In Re Ulrey, 511 B.R. 401 (Bankr. W.D. Va. 2014).

Photo Credit: milknosugar via photopin cc

{kind=link}

June 3, 2014

Engineer Personal Liability: Signed, Sealed & Delivered?

An engineer must obtain and maintain a Professional Engineer’s license from the APELSCIDLA Board to practice in the Commonwealth of Virginia. Pursuant to professional regulations, when an engineer, or other design professional, completes a set of drawings, he affixes his professional seal with the date and signature. His seal displays his professional license number. This finishing touch assures the reader, especially the owner and the builder, that the plans are ready to go.

If the project built according to the stamped plans fail, one would expect a claim against the engineering firm. With smaller design firms, the customer may only interact with one representative who handles everything. In such a case, what about engineer personal liability? On May 20, 2014, a federal judge in southwest Virginia issued an opinion in a case where the owner of a collapsing feed barn filed suit against an engineer after a barn he designed fell apart. The opinion shows the tension between the interests of freedom of contract and consumer protection in professional malpractice cases.

Ken McConnell hired Servinsky Engineering, PLLC to design a foundation for a barn on his farm. Mark Servinsky, a Virginia Professional Engineer, was its principal. The foundation constructed according to Servinsky’s plans failed, damaging the structure and tearing the fabric roof. The barn cannot be used safely. McConnell sued both the Servinsky firm and Mr. Servinsky personally. The engineering firm filed for bankruptcy protection. Mr. Servinsky filed a motion to have the personal claims against him dismissed.

McConnell alleged that Mr. Servinsky was personally liable for negligently performing the engineering work that resulted in an unusable barn. McConnell argued for liability on the grounds that Virginia law requires an engineer to affix his professional seal, signature and date to his drawings. Judge James Jones ruled that only the firm, and not the personal defendant, could be liable under the contract with McConnell. Here are a few takeaways in this judicial opinion:

- Privity of Contract: This is a legal principle whereby (except in limited situations) only the parties to a contract may sue other parties to the contract. Whether contractual privity is required in malpractice cases varies by profession and jurisdiction. If the customer sues for an engineer’s failure to meet the expectations set by the contract, then only the parties to the contract may be sued. Judge Jones does not address any arguments that McConnell’s contract was with anyone other than the engineering firm.

- Professional Regulations: Unless they specifically provide for personal liability, laws governing design professionals create duties surrounding licensure, not liability to consumers. The state board decides who can or cannot have a license.

- Professional Standards: If personal liability is difficult to prove and bankruptcy is available, what assurances does working with a professional provide to consumers? Judge Jones observed that in malpractice cases, the professional standards are implicit terms to any contract for services with a professional engineer. The professional standards fill in gaps as to the duty of care in performance of the contract. That is why negligence is discussed in these types of cases. The professional services firm cannot hide behind the absence of a specific term in the contract when there is a professional standard that articulates that duty.

Judge Jones dismissed McConnell’s claims against Mr. Servinsky personally, finding that the professional seal did not create professional duties to the customer above & beyond the professional services contract.

The Bankruptcy Court allowed McConnell’s suit against the engineering firm to proceed, since it was covered by insurance. That case is set to go to trial later this year. Servinsky’s engineer license provided McConnell with a potential remedy, but not by personal liability. The license was the prerequisite by which Servinsky to obtain a professional liability policy that may cover McConnell’s claim.

Case Citation: McConnell v. Servinsky Engineering, PLLC, 22 F.Supp.3d 610 (W.D. Va. 2014)

Photo Credit: Silver Smith, 2009″ Si1very via photopin cc (I could not find a fabric barn roof photo – this is actually of the Dallas Cowboys practice facility, not the facts of case discussed)

{kind=link}

May 29, 2014

What is a Revocable Transfer on Death Deed?

On May 20th I attended the 32nd Annual Real Estate Practice Seminar sponsored by the Virginia Law Foundation. Attorney Jim Cox gave a presentation entitled, Affecting Real Estate at Death: the Virginia Real Property Transfer on Death Act. Jim Cox presented an overview of this new estate planning tool that went into effect July 1, 2013.

Use of Transfer on Death (“TOD”) beneficiary designations for depository and retirement accounts is widespread. This 2013 Act allows owners of real estate to make TOD designations by recording a Revocable Transfer on Death Deed in the public land records.

The introduction of TOD Deeds is of interest to anyone involved in estate planning or real estate settlements. The following are 8 key aspects of this development in Virginia law:

- Not Really a “Deed.” A normal deed conveys an interest in real property to the grantee. A TOD Deed is a will substitute that becomes effective only if properly recorded and not revoked prior to death. The Act’s description of this instrument as a “deed” will likely be a source of confusion.

- Formal Requirements. A TOD Deed must meet the formal requirements of the statute in order to effect the intent of the owner. It must contain granting language (a.k.a. words of conveyance) appropriate for a TOD Deed. It is not effective unless recorded in land records prior to the death of the transferor. The statute contains an optional TOD Deed form. Due to the formal requirements, I cannot image advising someone to do one of these without a qualified attorney.

- Beneficiary Does Not Need to be Notified. Although a TOD Deed becomes public when filed, the transferor does not need to notify the recipient. The beneficiary may not learn about the designation until after the transferor’s death. At some point, the local government will change the addressee on the property tax bills.

- Freely Revocable. The transferor can revoke the TOD designation at any time prior to death. In fact, a TOD Deed cannot be made irrevocable. A revocation instrument must be recorded in land records.

- Unintended Title Problems. The Act takes pains to avoid creating title defects on the transferor’s title prior to death.

- Can be Disclaimed. The beneficiary can disclaim the transfer after the death of the transferor.

- Subject to Liens. Recording a TOD Deed does not trigger a due-on-sale clause in a mortgage. At the date of death, the beneficiary’s interest is subject to any enforceable liens on the property.

- Creditor Claims & Administration Costs. The beneficiary’s interest in the property is subject to any general claims of the transferor’s creditors or the expenses of the estate administration. Such claims may attach up to one year after the date of the transferor’s death. For this reason, the TOD beneficiary’s interest in the property or the proceeds of its sale will be uncertain until that 12 month period expires. However, taxing authorities, insurance companies, HOA’s and banks will expect payment prior to the end of those 12 months.

Each family has unique estate planning needs. The Va. Real Property TOD Act is a new gadget in the toolbox for crafting a plan that addresses individual desires and circumstances. Combining TOD Deeds with other estate planning tools such as wills and trusts requires careful integration to avoid unintended consequences. Estate planning and real estate practitioners will overcome any initial reluctance to use of TOD Deeds as they become subject to the test of time.

If you learn that you are the beneficiary of a TOD deed and are uncertain as to your rights and responsibilities with respect to the property, contact an experienced real estate attorney.

{kind=link}

May 21, 2014

Dealing With Trust Issues: Fiduciary Duties of Foreclosure Trustees

In Virginia, unlike some other states, a foreclosure is a transaction and not necessarily a court proceeding. A trustee appointed by the lender auctions the property. The proceeds of the sale must be applied to reduce the outstanding loan amount and transaction costs. A Trustee has special duties to the parties as their “fiduciary.” What are the fiduciary duties of foreclosure trustees?

At real estate closings, settlement attorneys present borrowers with a document entitled “Deed of Trust.” In this document, the borrower pledges the purchased property as collateral. The Deed of Trust provides the legal framework for the lender to pursue foreclosure in a default. It also procedurally protects the borrower’s property rights. When the lender records the Deed of Trust in the land records, a lien encumbers the property until the debt is released. The Deed of Trusts names one or more persons as Trustees for the property. It describes the borrower as the creator of the trust and the bank as the beneficiary. If the borrowers avoid falling into persistent default of their loan obligations, this trust language is largely irrelevant.

If the borrower experiences economic hardship and falls behind on their payments, however, they will begin to receive notices referencing the Deed of Trust. The bank may appoint a Substitute Trustee to handle the foreclosure. The culmination of the foreclosure process is the Foreclosure Trustee’s public auction of the property to satisfy the distressed loan. What does the foreclosure process have to do with trusts and trustees? Generally, under Virginia law, a breach of a trustee’s duties gives rise to a Breach of Fiduciary Duty legal claim. Lawyers like to pursue these claims because they may impose duties and remedies not articulated in the contract. Does this trust relationship give the homeowner greater or fewer protections against breaches by the bank’s agents during the process?

On May 16, 2014, I posted an article about the materiality of technical errors committed by the mortgage investors in the foreclosure process. That post focused on two new April 2014 court opinions providing some guidance on what remedies borrowers may have for those errors. Those new court opinions also provide fresh guidance about fiduciary duties of foreclosure trustees. Today’s blog post is about dealing with trust issues in foreclosure.

Bonnie Mayo v. Wells Fargo Bank & Samuel I. White, PC:

The Deed of Trust on Bonnie Mayo’s Williamsburg home listed Wells Fargo Bank as the “beneficiary” and the foreclosure law firm Samuel I. White, PC, as the Trustee. Mayo’s post-foreclosure sale lawsuit alleged that the White Firm breached its fiduciary duties to the borrower. For example, Mayo’s Deed of Trust required the lender to state in written default notices that she may sue to assert her defenses to foreclosure. The lender’s notices did not advise her of this, and she did not sue until after the foreclosure occurred. The Federal Judge considering her claims noted that there is conflicting legal authority on the extent to which a foreclosure Trustee can be sued for Breach of Fiduciary Duty. In his April 11, 2014 opinion, Judge Jackson observed that under Virginia law, a Foreclosure Trustee is a fiduciary for both the borrowing homeowner and the mortgage investor. While courts impose those duties on Foreclosure Trustees set forth in the Deed of Trust, they are reluctant to impose all general trust law principles.

Judge Jackson concluded that in addition to those duties set forth or incorporated into the Deed of Trust, the only other imposed on Trustees is the duty of impartiality. For example a foreclosure sale must be set aside where a trustee failed to refrain from placing himself in a position where his personal interests conflicted with the interests of the borrower and the lender. For example, the Trustee may not purchase the auctioned property himself or assist the bank in setting its bid. The Federal Judge dismissed Ms. Mayo’s Breach of Fiduciary Duty claims against the White Law firm, since impartiality was not adequately pled in the lawsuit.

Squire v. Virginia Housing & Development Authority:

In an April 17, 2014 opinion, the Supreme Court of Virginia focused on the limited nature of a Foreclosure Trustee’s powers. In this case, the Deed of Trust required the lender to try to conduct a face-to-face meeting with the borrower between the default and the foreclosure. The lender’s Trustee foreclosed, even though the lender did not make such an effort. The Court observed that the trustee’s authority to foreclose is set forth in the Deed of Trust. The Trustee’s power to conduct the sale does not accrue until the specified conditions are met. The borrowers’ failure to make monthly payments does not constitute a waiver of their right to expect the lender’s appointee to follow the rules. The fact that the borrower is in default does not authorize the mortgage investor and the trustee to disregard the Borrower’s protections set forth in the Deed of Trust and any incorporated regulations.

This holding is consistent with Virginia’s practice of conducting foreclosures out of court. The procedures set forth in the deed of trust provide the lender with a means of selling the property without the time & expense of a judicial sale. If the procedural nature of those rights is not preserved, then foreclosure disputes will go to court more often, depriving the lenders of the convenience of non-judicial foreclosure.

Ms. King alleged that the Foreclosure Trustee breached its fiduciary duty by conducting the sale prior to a required face-to-face meeting with the borrower. The Supreme Court of Virginia found that the Breach of Fiduciary duty claim was improperly dismissed by the Norfolk judge. The Court sent the case back down for consideration of damages.

These two new court opinions show how breach of fiduciary duty claims against foreclosure trustees require legal interpretation of the deed of trust. If the lender and trustee digress from its procedures, impartiality may be easier to prove.

Discussed Case Opinions:

Mayo v. Wells Fargo Bank, No. 4:13-CV-163 (E.D.Va. Apr. 11, 2014)(Jackson, J.)

Squire v. Virginia Housing Development Authority, 287 Va. 507 (2014)(Powell, J.)

Credits: Trust Arch photo credit: Lars Plougmann via photopin cc Williamsburg photo credit: Corvair Owner via photopin cc (for illustrative/informational purposes only. Depicts colonial Williamsburg, not Ms. Mayo’s home)

{kind=link}

May 16, 2014

What Difference Does It Make? Technical Breaches By Banks in Foreclosure

If a bank makes a technical error in the foreclosure process, what difference does it make? This blog post explores new legal developments regarding the materiality of breaches of mortgage documents. Residential foreclosure is a dramatic remedy. A lender extended a large sum of credit. Borrowers stretch themselves to make a down payment, monthly payments, repairs, association dues, taxes, etc. If financial hardships present obstacles to borrowers making payments, usually they will do what they can to keep their home.

In order to foreclose, lenders must navigate a complex web of provisions in the loan documents and relevant law. Note holders frequently commit errors in processing a payment default through a foreclosure sale. Sometimes these breaches are flagrant, such as foreclosing on a property to which that lender does not hold a lien. Usually they are less significant in the prejudice to the borrower’s rights. For example, written notices may not follow contract provisions or regulations verbatim, or a notice went out a day late or by regular mail instead of certified mail. Regardless of their significance, these rules were either willingly adopted by the parties or represent public policies reduced to law.

When homeowners challenge foreclosures in Court, lenders frequently argue in defense that the errors committed by the bank in the foreclosure process are not material. One could express this argument in another way by quoting the title lyric to British band The Smiths’ 1984 song, “What difference does it make?” The lenders typically highlight that the borrowers fell behind on their payments, did not come current, and do not have a present ability to come current on their loans. Borrowers face an uphill battle convincing judges to set aside or block foreclosure trustee sales or award money damages for non-material breaches. However, last month, two new court opinions illustrate a trend towards allowing remedies to homeowners for technical breaches. A relatively small award of money damages may not give homeowners their house back, but it may provide some consolation to the borrower and provide an incentive to mortgage investors, servicers and foreclosure trustees to strengthen their compliance programs.

When homeowners challenge foreclosures in Court, lenders frequently argue in defense that the errors committed by the bank in the foreclosure process are not material. One could express this argument in another way by quoting the title lyric to British band The Smiths’ 1984 song, “What difference does it make?” The lenders typically highlight that the borrowers fell behind on their payments, did not come current, and do not have a present ability to come current on their loans. Borrowers face an uphill battle convincing judges to set aside or block foreclosure trustee sales or award money damages for non-material breaches. However, last month, two new court opinions illustrate a trend towards allowing remedies to homeowners for technical breaches. A relatively small award of money damages may not give homeowners their house back, but it may provide some consolation to the borrower and provide an incentive to mortgage investors, servicers and foreclosure trustees to strengthen their compliance programs.

Content of Written Notices Required by Mortgage Documents:

On June 13, 2010, Wells Fargo Bank sent Bonnie Mayo a letter telling her he was in default on her mortgage on her Williamsburg residence. The letter indicated that if she failed to cure within 30 days, Wells Fargo would proceed with foreclosure. The letter informed her that, “[i]f foreclosure is initiated, you have the right to argue that you did keep your promises and agreements under the Mortgage Note and Mortgage, and to present any other defenses you may have.” However, the Mortgage required the lender to state in the written notice the borrower’s “right to reinstate after acceleration and right to bring a court action to assert the non-existence of a default or any other defense of Borrower to acceleration and sale.” Ms. Mayo’s notice did not include this language. She did not bring a lawsuit until after the date of the foreclosure sale.

In her post-foreclosure lawsuit, Mayo alleged (among other claims) that this breach entitled her to rescind the foreclosure and receive money damages. Wells Fargo moved to dismiss this claim on the grounds that the difference between the contractually required language and the actual letter was immaterial. In an April 11, 2014 opinion, Judge Raymond Jackson observed that just because a breach is non-material does not mean it is not a breach at all. He reached a conclusion contrary to a relatively recent opinion of another judge in the U.S. District Court for the Eastern District of Virginia.

Virginia courts recognize claims to set aside foreclosure sales for “weighty” reasons but not “mere technical” grounds. Judge Jackson suggested that the bar may be higher for a homeowner to set aside a foreclosure sale after it occurs than to block it from happening in the first place. The Court declined to dismiss this claim on the sufficiency of the notices. Judge Jackson found that the materiality of this breach was a factual dispute requiring additional facts and argument to resolve.

A foreclosure is less susceptible to legally challenge after a subsequent purchaser goes to closing. Thus, the bank’s omission of language informing the borrower of her right to sue prior to the foreclosure carried a heightened potential for prejudice. Whether Ms. Mayo had a likelihood of prevailing in an earlier-filed lawsuit is a different story.

Failure to Conduct a Face-to-Face Meeting Prior to Foreclosure:

In 2002, Kim Squire King financed the purchase of a home in Norfolk, Virginia, with a Virginia Housing Development Authority mortgage. Her loan documents incorporated U.S. Department of Housing & Urban Development regulations requiring a lender to make reasonable efforts to arrange a face-to-face interview with the borrower between default and foreclosure. Loss of employment caused King to go into default on her VHDA loan in March 2010. VHDA never offered King a face-to-face meeting. VHDA instituted foreclosure wherein the trustee sold King’s property to a third-party.

King filed a lawsuit seeking money damages and an order rescinding the foreclosure sale. The judge in Norfolk agreed with defense arguments that the error was not grounds to set aside the completed foreclosure or award compensatory damages. The court dismissed the lawsuit. Squire appealed to the Supreme Court of Virginia. The Justices upheld the dismissal of her request to set aside the completed foreclosure sale. The lawsuit failed to allege facts sufficient to show that the sale was fraudulent or grossly inadequate.The Supreme Court distinguished King’s situation from legal precedents where the borrower filed suit prior to the foreclosure. Surprisingly, the Court found that the trial judge erred in dismissing King’s claim for money damages arising out of the failure to arrange the face to face meeting. The Justices remanded the case to proceed on the damages issue.

When mortgage servicers and foreclosure trustees commit technical errors, what difference does it make? These new legal decisions show increasingly nuanced analysis of these particular issues. The materiality of the lender’s breach depends on a number of factors, including:

- The borrower’s apparent ability to reinstate the loan. If it is unlikely that the homeowner will get back on track, denying the bank foreclosure makes less sense.

- Did the borrower file suit before or after the foreclosure sale? A lawsuit can delay a foreclosure until the borrowers enforce their rights under the loan documents and incorporated regulations. However, unless the borrowers have a strategy to work-out the distressed loan or otherwise favorably dispose of the property, a pre-foreclosure lawsuit may only delay.

- The relationship between the technical error and the relief requested by the borrower. For example, if the loan documents require a notice to go out by certified mail and it only goes out by first class mail, but the borrower received it anyway, then there isn’t any prejudice.

- Money damages suffered by the borrower that arose out of the technical breach. Borrowers seek to keep their homes and to pay according to their abilities. The U.S. District Court for the Eastern District of Virginia and the Supreme Court of Virginia show an increasing willingness to hold lenders monetarily responsible for prejudicial lender breaches in the foreclosure process. A legal claim that partially offsets the lender’s judgment for the balance of the loan post-foreclosure may provide some consolation but may not avoid bankruptcy.

Discussed Case Opinions:

Mayo v. Wells Fargo Bank, No. 4:13-CV-163 (E.D.Va. Apr. 11, 2014)(Jackson, J.)

Squire v. Virginia Housing Development Authority, 287 Va. 507 (2014)(Powell, J.)

photo credit: Fabio Bruna via photopin cc

{kind=link}

May 6, 2014

Mortgage Fraud Shifts Risk of Decrease in Value of Collateral in Sentencing

On March 5, 2014, I blogged about the oral argument before the U.S. Supreme Court in U.S. v. Benjamin Robers, a criminal mortgage fraud sentencing appeal. At stake was how Courts should credit the sale of distressed property in calculating restitution awards. The U.S. Court of Appeals for the Seventh Circuit interpreted the Mandatory Victims Restitution Act to apply the sales price obtained by the bank selling the property post foreclosure as a partial “return” of the defrauded loan proceeds. Robers appealed, arguing that he was entitled to the Fair Market Value of the property at the time of the foreclosure auction. According to Robers, the mortgage investors should bear the risk of market fluctuations post-foreclosure because they control the disposition of the collateral. See Mar. 5, 2014, How Should Courts Determine Mortgage Fraud Restitution?

Yesterday, the Supreme Court affirmed the re-sale price approach in a unanimous decision. The Court observed that the perpetrators defrauded the victim banks out of the purchase money, not the real estate. The foreclosure process did not restore the “property” to the mortgage investors until liquidation at re-sale.

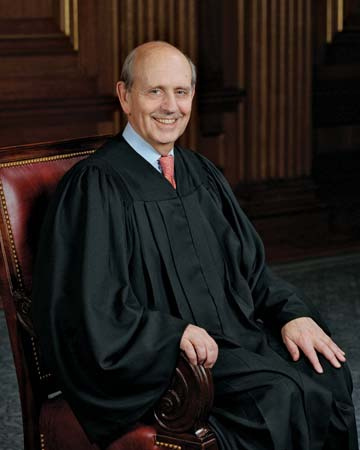

The Court focused on defense arguments that the real estate market, not Robers, caused the decrease in value of collateral between the time of the foreclosures and the subsequent bank sales. Justice Stephen Breyer wrote that:

Fluctuations in property values are common. Their existence (through not direction or amount) are foreseeable. And losses in part incurred through a decline in the value of collateral sold are directly related to an offender’s having obtained collateralized property through fraud.

Breyer distinguished “market fluctuations” from actions that could break the causal chain, such as a natural disaster or decision by the victim to gift the property or sell it to an affiliate for a nominal sum. See Lance Rogers, May 6, 2014, BNA U.S. Law Week, “Justices Clarify that Restitution ‘Offset’ is Gauged at Time Lender Sells Collateral.”

Falsified mortgage applications cause a lender to make a loan that it would not otherwise extend. A restitution award mirroring what the lender would receive in a civil deficiency judgment is inadequate. The defendant’s conduct opened the door for the Court to shift the risk of post-foreclosure market fluctuation from the bank to the borrower. Robers did not single-handedly render the local real estate market illiquid. However, as Justice Sonia Sotomayor mentions in her concurrence, real estate takes time to liquidate. These banks did not unreasonably delay the liquidation process. The Court opinion did not mention the prominent role of origination fraud in the subprime mortgage crisis. The Supreme Court’s unanimous decision strongly rejected defense arguments that downward “market fluctuations” severed the causal connection between the origination fraud and the depressed sales prices obtained by the lenders.

The Court did not discuss the original purchase prices for Robers’ two homes. In many mortgage fraud schemes, loan officers find “straw purchasers” such as Mr. Robers for sellers who agree to provide kickbacks on the inflated sales prices. See Mar. 15, 2009, Milwaukee Journal-Sentinel, “Amid Subprime Rush, Swindlers Snatched $4 Million.” The perpetrators do not disclose these kickbacks to the lenders. The mortgage originators also receive origination fees from the lenders on the fraudulent closings. Under this arrangement, the purchase price will naturally reflect the highest sales price the bank’s appraiser will support. The bank is defrauded both by the fictitious qualifications of the borrower and the exaggerated sales prices.

U.S. v. Robers may result in stricter, more consistent restitution awards in mortgage fraud cases. I wonder how it will be applied in cases where the defendant presents stronger evidence that the victims acted unreasonably in liquidating the property. The opinion seems to leave discretion to District Courts to determine whether a bank’s conduct or omissions breaks the connection between the mortgage fraud and the sales price.

{kind=link}

May 2, 2014

Sterling v. Stiviano: Spouse Sues Paramour Over Title to Property

Earlier this week, the National Basketball Association imposed a lifetime ban on Donald Sterling, owner of the Los Angeles Clippers. Adventuress Vanessa Stiviano recorded racist and demeaning statements made by Sterling about Basketball Hall of Famer Earvin “Magic” Johnson. The recordings subsequently leaked to the public.

In 1991, I watched the first NBA Finals for the first time. Magic Johnson led the Lakers against Michael Jordan’s Chicago Bulls. The 1991 Finals made me a basketball fan. Magic was one of my favorite professional athletes. The news about Don Sterling is offensive and bizarre. Why is this scandal happening?

On March 7, 2013, Sterling’s wife, Rochelle, filed a lawsuit against Ms. Stiviano. The lawsuit alleges that Stiviano seduced Don for money. According to Rochelle, Stiviano used marital funds to purchase a $1.8 Million dollar duplex home in Los Angeles in December 2013. Rochelle seeks a court order reforming the deed to identify herself and her husband as the proper owners.

The LA Times reports that Mr. Sterling told Clippers President Andy Roeser that Stiviano said that she would “get even” with Rochelle for filing the lawsuit. Apr. 26, 2014, Bettina Boxall, Sterling’s Wife Describes Alleged Mistress as Gold Digger in Lawsuit. I wonder if Stiviano has additional embarrassing Sterling recordings that she has not yet leaked. There is a controversy over whether the recordings were consensual. How are these leaked recordings related to the lawsuit?

Rochelle alleges that Donald Sterling provided the money for Stiviano to purchase the duplex, “with the understanding that the Property would be owned by [Donald and Rochelle Sterling] and title would vest in the name of [Rochelle] and D. Sterling.” Curiously, Donald is not a Plaintiff or Defendant to this lawsuit where the spouse sues paramour. Rochelle alleges that, “D. Sterling either gifted said Property to Stiviano, without the knowledge, consent or authorization of Plaintiff, or, in the alternative, Stiviano fraudulently and wrongfully caused title to the Property to vest in her name.”

Stiviano’s response focuses on the confusing and contradictory nature of Rochelle’s pleading. Her lawyer makes a few key arguments on demurrer:

- The transfers made from Donald to Stiviano were gifts.

- Rochelle and Donald are not in divorce proceedings.

- Rochelle does not allege that any of the transfers were thefts.

- Mr. Sterling is an, “on the top of his game infamous real estate mogul.”

- Rochelle knew of Donald’s reputation for “gold plated dalliances” in general and his relationship with Stiviano in particular.

Don Sterling’s health history is an issue. ESPN reports today that Mr. Sterling has prostrate cancer.

I try to avoid predicting the outcome of pending motions, especially those in California, where I do not practice law. Can a California Judge base a ruling on new facts introduced by a defendant on demurrer?

Rochelle alleges that she and Donald are the real owners of the duplex because either:

- Donald and his wife were supposed to be the grantees on the deed, and somehow the name got switched to Stiviano; or

- Donald secreted the funds to Stiviano out of the family estate without Rochelle’s knowledge.

These allegations seem contradictory. In the first case, there was an intention for the paramour to be the nominal purchaser for the benefit of the husband and wife. Did Rochelle condone Don’s relationship with Stiviano? The alternative alleges waste of marital assets, but outside a divorce proceeding. The “constructive trust” remedy sought by Rochelle is a flexible one. However, a spouse usually cannot invalidate transfers to a “other woman” absent theft, fraud, incapacity or other conduct that voids the intent of the philanderer.

This demurrer is set for hearing on July 8, 2014. Many things could happen before then. Don Sterling’s health is an issue. The media will shift their focus to other sports after the NBA Finals and Draft wrap up in late June. Will the NBA successfully force Sterling to sell the Clippers? His lawyers will research the admissibility of the Stiviano tapes thoroughly. Regardless as to how deep they go into the playoffs, the Clippers will have an eventful off-season.

{kind=link}

April 16, 2014

Unlicensed Real Estate Agent Costs Brokerage $6.6 Million Commission

What tasks can real estate brokerages assign to employees lacking a real estate license? What risks does a brokerage run from allowing unlicensed agents to manage relationships with clients and other parties to the transaction? On April 4, 2014, Judge Anthony Trenga decided that a prominent commercial broker forfeited a $6.6 million dollar commission because a leading member of its team lacked a Virginia salesperson’s license. This blog post discusses how the brokerage lost the commission on account of the unlicensed manager.

The Hoffman Town Center is a 56 acre mixed-use development in Alexandria, Virginia. (Yours truly lived in Alexandria for 9 years. AMC Hoffman was my local movie theater. I ran across the finish line in the George Washington’s Birthday 10K race at the Town Center.)

The Landlord, Hoffman Family, LLC, sought office tenants for the development. In August 2007, Hoffman retained Jones Lang LaSalle Americas, Inc. (“JLL”) as its leasing agent. JLL itself has a valid Virginia broker’s license.

In October 2007, Arthur M. Turowski retired from the U.S. General Services Administration. JLL hired him as a Senior Vice President and assigned him to manage the Hoffman account. Torowski saw an opportunity to lease the property to the National Science Foundation. He marketed the property to the GSA, who successfully bid on behalf of the NSF. Turowski negotiated with GSA and city officials. He signed documents on behalf of JLL. In May 2013, Turowski achieved a $330 million lease for his client from the federal government. The NSF will be an anchor tenant in the development. See Jonathan O’Connell, Wash. Post, Judge Rules for Developer in $6.6 million National Science Foundation Suit.

Mr. Turowski helped Hoffman outshine other suitors and land a sought-after tenant. Unfortunately JLL made one oversight: Turowski lacked a real estate agent’s license while performing the work. Hoffman discovered this fact while defending a lawsuit brought by JLL for payment of the $6.6 million dollar commission (JLL rejected Hoffman’s offer of $1 million).

In its ruling, the U.S. District Court for the Eastern District of Virginia discussed the broad scope of activities for which Virginia law requires a license:

1. Activities Requiring a Licence. The legal definition of “real estate salesperson” is “clearly intended to capture the realities and breadth of activities that make up the leasing process.” This strengthens the real estate sales profession by recognizing business realities and restricting the scope of activities unlicensed persons may engage in. Va. Code Sect. 54.1-2101 “Negotiation” is a broad professional activity not limited to agreeing to a property and a price and signing documents.

2. Activities Not Requiring a License. The Virginia Code provides for a narrow set of activities an employee of a broker may do without a license, such as (a) showing apartments if the employee also works on the premises (b) providing prospective tenants with information about properties, (c) accepting applications to lease and (d) accepting security deposits and rents. Va. Code Sect. 54.1-2103(C). These do not include relationship management and negotiation on behalf of a client. JLL’s lawyers argued that Turowski did not engage in activities requiring a license. If that was the case, what licensee-level work earned the commission? The opinion notes that GSA opted to deal with some matters with Hoffman directly because JLL represented other landlords competing for the NSF tenant.

Judge Trenga found that Virginia law required Turowski to hold a license to work under JLL’s agreement with the Hoffman Family. Since he did not, the Court denied JLL’s request for any portion of the commission. The Court observed that a realtor agreement between an unlicensed agent and a client is void. JLL did have a broker’s license and Hoffman’s contract was with JLL. However, Virginia law does not allow brokers to use unlicensed employees as sales persons. The Court decided that JLL’s use of Turowski voided its commission. Even if a listing agreement is valid at the time it was signed, if the brokerage performs under it through an unlicensed salesperson, that performance violates public policy and voids the commission.

The opinion does not discuss whether any other JLL personnel worked on the Hoffman account. I wonder whether JLL would have received a monetary award if licensed sales persons performed some of the work? Perhaps the outcome would have been less harsh if Turowski was not the leader?

Could a licensed real estate sales persons have achieved a greater result for Hoffman? The opinion does not discuss specific damages that arose out of JLL’s failure to use licensed sales persons in performance of the agreement. The underlying agreement was not per se void. In the end, Hoffman got a $330 million lease negotiated by an (unlicensed) agent with deep familiarity with the agency he negotiated with. Unless the verdict is disturbed on appeal, Hoffman does not have to pay anything except its attorney’s fees defending this suit.

Daniel Sernovitz of the Washington Business Journal observes that this litigation gave both the developer and the broker black eyes. Sernovitz points out that JLL’s lawsuit cast a cloud over the project. The possibility of reversal on appeal keeps a shadow of doubt on whether Hoffman will have an extra $6.6 million to help finance the next phase in the development. Lastly, the Hoffman-JLL relationship was mutually beneficial prior to this fee dispute. JLL’s relationships could procure additional tenants. Hoffman may have to rely upon other brokerages moving forward.

Do you think that use of an unlicensed real estate agent presents the same risk to residential brokers?

case cite: Jones Lang LaSalle Americas, Inc. v. Hoffman Family, LLC, No. 1:13-cv-01011-AJT, 2014 WestLaw 1365793 (E.D. Va. Apr. 4, 2014)(Trenga, J.).

{kind=link}